All Categories

Featured

Table of Contents

The method has its very own benefits, yet it also has issues with high fees, intricacy, and much more, leading to it being considered as a rip-off by some. Infinite banking is not the very best plan if you require only the investment part. The limitless financial idea focuses on using whole life insurance coverage plans as a monetary device.

A PUAR enables you to "overfund" your insurance coverage right up to line of it ending up being a Changed Endowment Agreement (MEC). When you use a PUAR, you swiftly boost your cash money value (and your survivor benefit), therefore enhancing the power of your "bank". Additionally, the even more cash value you have, the higher your passion and dividend payments from your insurance policy firm will certainly be.

With the increase of TikTok as an information-sharing platform, economic suggestions and approaches have actually found an unique means of dispersing. One such approach that has been making the rounds is the limitless banking idea, or IBC for brief, garnering recommendations from celebrities like rap artist Waka Flocka Flame - Private banking strategies. Nonetheless, while the approach is presently prominent, its origins trace back to the 1980s when economic expert Nelson Nash introduced it to the globe.

Infinite Wealth Strategy

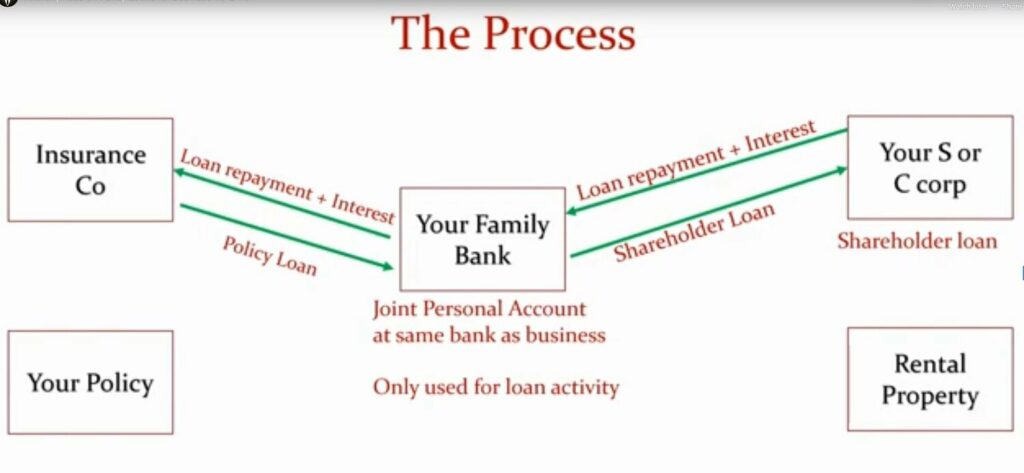

Within these plans, the money value grows based upon a price set by the insurance company. Once a considerable cash worth accumulates, insurance holders can acquire a cash worth funding. These financings vary from traditional ones, with life insurance policy functioning as security, implying one might shed their coverage if borrowing exceedingly without sufficient cash worth to support the insurance costs.

And while the allure of these plans appears, there are inherent limitations and threats, requiring diligent money value monitoring. The strategy's authenticity isn't black and white. For high-net-worth people or service proprietors, especially those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance development could be appealing.

The allure of infinite financial doesn't negate its challenges: Expense: The foundational requirement, a long-term life insurance policy policy, is more expensive than its term equivalents. Eligibility: Not everybody receives whole life insurance policy as a result of strenuous underwriting procedures that can omit those with specific wellness or way of life conditions. Complexity and risk: The elaborate nature of IBC, coupled with its dangers, might discourage several, specifically when less complex and less dangerous choices are available.

What do I need to get started with Policy Loan Strategy?

Assigning around 10% of your monthly revenue to the policy is just not possible for lots of people. Using life insurance policy as a financial investment and liquidity source calls for technique and tracking of plan cash value. Seek advice from a monetary expert to figure out if limitless financial lines up with your concerns. Part of what you read below is merely a reiteration of what has actually currently been stated over.

Prior to you get yourself into a situation you're not prepared for, know the complying with first: Although the idea is commonly sold as such, you're not really taking a funding from yourself. If that held true, you would not need to repay it. Rather, you're obtaining from the insurance provider and need to repay it with passion.

Some social media sites blog posts recommend making use of cash money worth from whole life insurance coverage to pay for charge card financial obligation. The idea is that when you settle the financing with interest, the amount will certainly be sent out back to your investments. That's not just how it functions. When you pay back the funding, a part of that rate of interest goes to the insurance provider.

Can anyone benefit from Infinite Banking Cash Flow?

For the very first numerous years, you'll be settling the commission. This makes it exceptionally difficult for your policy to accumulate worth during this time. Entire life insurance coverage expenses 5 to 15 times more than term insurance. Lots of people merely can't afford it. Unless you can afford to pay a couple of to a number of hundred bucks for the following years or more, IBC won't function for you.

Not everybody needs to depend only on themselves for economic safety and security. Cash value leveraging. If you call for life insurance coverage, here are some useful pointers to think about: Think about term life insurance coverage. These policies give protection during years with substantial monetary commitments, like home mortgages, trainee lendings, or when taking care of kids. Make sure to search for the very best price.

How do I qualify for Infinite Banking In Life Insurance?

Think of never having to stress over financial institution finances or high rates of interest once again. What if you could borrow cash on your terms and build wide range concurrently? That's the power of limitless banking life insurance policy. By leveraging the cash value of whole life insurance policy IUL policies, you can expand your wide range and obtain cash without depending on conventional banks.

There's no set car loan term, and you have the flexibility to choose on the payment routine, which can be as leisurely as repaying the loan at the time of fatality. This adaptability expands to the servicing of the financings, where you can opt for interest-only repayments, maintaining the loan balance flat and workable.

How do interest rates affect Infinite Banking Benefits?

Holding money in an IUL fixed account being credited rate of interest can usually be much better than holding the cash on deposit at a bank.: You've constantly desired for opening your very own bakery. You can borrow from your IUL plan to cover the initial costs of renting out a space, buying equipment, and hiring team.

Individual lendings can be gotten from conventional financial institutions and cooperative credit union. Right here are some essential points to take into consideration. Credit rating cards can provide an adaptable method to obtain money for very short-term durations. Nonetheless, obtaining cash on a charge card is usually very expensive with yearly percent rates of interest (APR) usually reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Infinite Banking Concept And Cash Value Life Insurance

Infinite Banking Nelson Nash

Infinite Banking Center