All Categories

Featured

Table of Contents

The method has its very own benefits, yet it also has problems with high charges, intricacy, and much more, leading to it being pertained to as a rip-off by some. Boundless banking is not the most effective plan if you need just the financial investment element. The limitless banking principle revolves around making use of whole life insurance policies as a financial device.

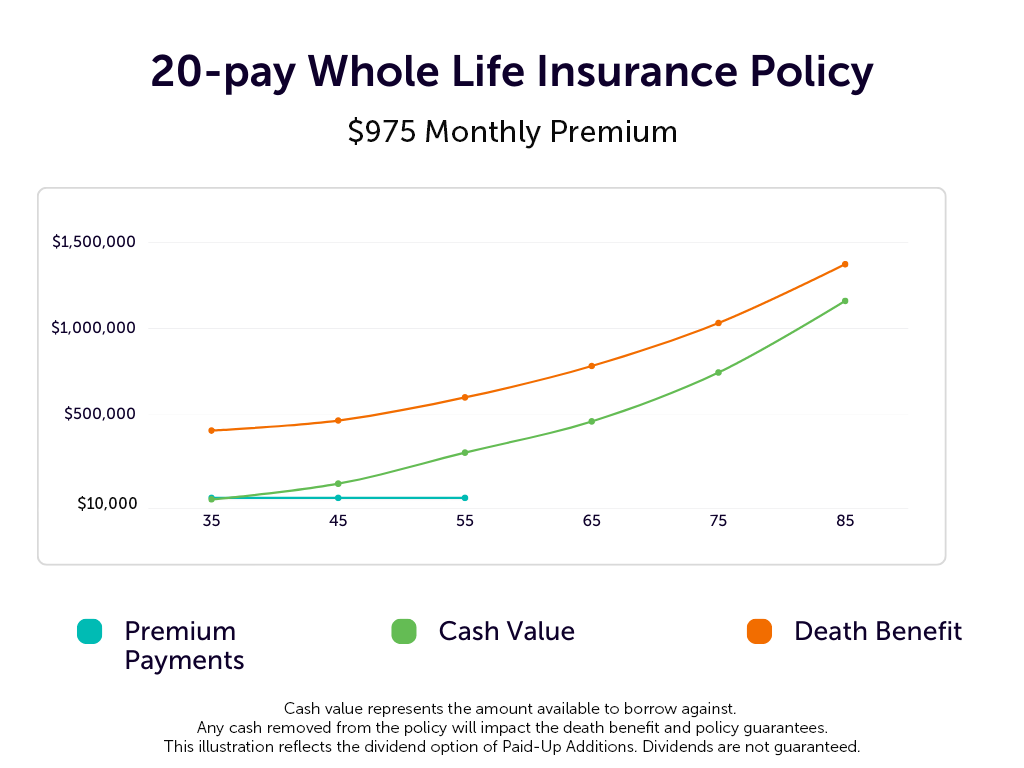

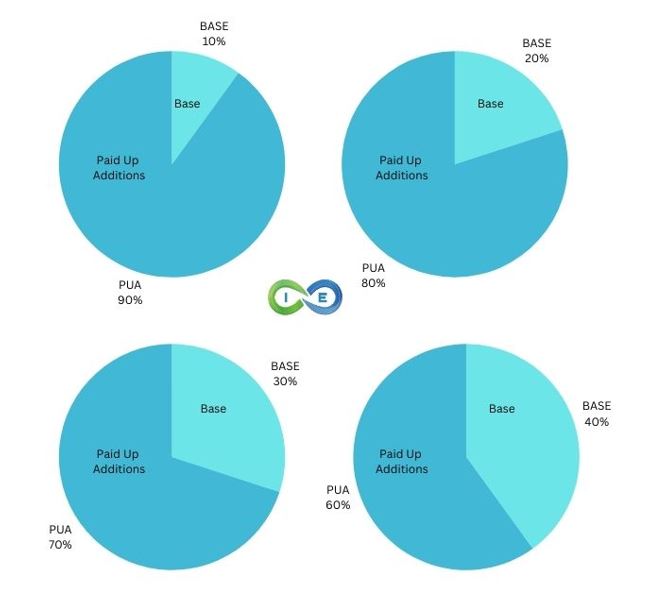

A PUAR allows you to "overfund" your insurance coverage right as much as line of it coming to be a Customized Endowment Agreement (MEC). When you make use of a PUAR, you quickly raise your cash money value (and your death benefit), therefore raising the power of your "financial institution". Further, the even more money worth you have, the better your interest and dividend payments from your insurer will be.

With the surge of TikTok as an information-sharing platform, economic recommendations and approaches have actually located an unique method of dispersing. One such method that has been making the rounds is the boundless banking concept, or IBC for short, gathering endorsements from stars like rapper Waka Flocka Flame - Cash flow banking. Nevertheless, while the technique is presently prominent, its origins map back to the 1980s when financial expert Nelson Nash presented it to the globe.

What are the most successful uses of Infinite Banking Wealth Strategy?

Within these plans, the money worth expands based upon a price set by the insurance company. Once a substantial cash money value accumulates, insurance policy holders can get a cash money worth finance. These lendings vary from conventional ones, with life insurance policy serving as security, meaning one might lose their protection if loaning exceedingly without ample cash money worth to sustain the insurance policy costs.

And while the appeal of these plans appears, there are inherent limitations and dangers, requiring diligent cash money worth surveillance. The strategy's authenticity isn't black and white. For high-net-worth individuals or company owner, especially those making use of techniques like company-owned life insurance coverage (COLI), the advantages of tax breaks and substance growth might be appealing.

The appeal of limitless banking doesn't negate its difficulties: Price: The fundamental requirement, an irreversible life insurance policy, is more expensive than its term equivalents. Qualification: Not everybody receives entire life insurance policy as a result of rigorous underwriting processes that can exclude those with specific health and wellness or way of life problems. Intricacy and danger: The complex nature of IBC, coupled with its dangers, might hinder many, specifically when simpler and much less risky alternatives are available.

Who can help me set up Infinite Banking In Life Insurance?

Assigning around 10% of your month-to-month earnings to the plan is just not practical for most individuals. Using life insurance policy as a financial investment and liquidity source calls for technique and monitoring of policy money value. Get in touch with an economic consultant to establish if unlimited financial straightens with your top priorities. Part of what you read below is merely a reiteration of what has actually already been stated over.

Before you get yourself into a scenario you're not prepared for, know the following first: Although the principle is commonly marketed as such, you're not actually taking a financing from on your own. If that were the case, you would not need to repay it. Instead, you're borrowing from the insurance provider and need to repay it with interest.

Some social media blog posts suggest making use of cash value from whole life insurance coverage to pay down credit report card financial obligation. When you pay back the car loan, a section of that passion goes to the insurance coverage company.

What are the common mistakes people make with Infinite Banking For Retirement?

For the very first several years, you'll be settling the compensation. This makes it incredibly difficult for your policy to build up value during this moment. Whole life insurance policy prices 5 to 15 times extra than term insurance coverage. A lot of people just can not afford it. So, unless you can pay for to pay a few to a number of hundred bucks for the next decade or even more, IBC won't benefit you.

Not every person ought to count solely on themselves for economic security. Generational wealth with Infinite Banking. If you require life insurance, here are some useful suggestions to think about: Think about term life insurance policy. These policies offer insurance coverage during years with significant financial responsibilities, like home mortgages, pupil financings, or when caring for young youngsters. Make certain to search for the very best price.

Is there a way to automate Infinite Wealth Strategy transactions?

Picture never ever having to stress regarding bank fundings or high interest prices once again. That's the power of infinite banking life insurance policy.

There's no collection funding term, and you have the freedom to select the payment routine, which can be as leisurely as settling the funding at the time of death. This flexibility encompasses the maintenance of the car loans, where you can decide for interest-only payments, keeping the loan equilibrium level and convenient.

What are the risks of using Infinite Banking Wealth Strategy?

Holding money in an IUL repaired account being credited passion can usually be far better than holding the cash on down payment at a bank.: You've constantly imagined opening your own bakeshop. You can obtain from your IUL policy to cover the first expenses of renting an area, purchasing devices, and working with team.

Personal lendings can be obtained from typical banks and cooperative credit union. Here are some bottom lines to take into consideration. Charge card can provide a versatile means to obtain cash for very short-term periods. Nevertheless, borrowing money on a bank card is generally extremely pricey with interest rate of interest (APR) usually reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Infinite Banking Concept And Cash Value Life Insurance

Infinite Banking Nelson Nash

Infinite Banking Center